5 Red Flags to Watch for When Your Property Manager Sends You Owner Statements

Owner statements often hide more than they show. Learn the 5 red flags — from unsupported expenses to expired leases — every rental property owner should check.

FINANCIAL REPORTINGRENTAL PROPERTY ACCOUNTINGRENTAL REAL ESTATE

Aditya Kumar

7/3/20268 min read

4. Track your cash position over the year

Pull your cash flow statement and do a simple check: how much cash did you have at the start of the year, and how much do you have now — say, this June or July? Is that a steady decline, month after month? Or is it just stagnant, sitting flat with no real movement in either direction?

This one number, tracked over time, tells you more than almost anything else in your reporting, precisely because it's hard to dress up. Individual line items can look reasonable in isolation — a repair here, a slightly lower month of rent there — while the cumulative trend tells a completely different story. A property that's slowly bleeding cash quarter after quarter is telling you something real, even if nobody can point to one specific bad decision that caused it. Likewise, a property that never seems to build any reserve at all, year after year, despite reportedly healthy income, deserves a direct question: where is the money actually going?

This doesn't require a complicated model. Pull the cash balance from twelve months ago, pull it from today, and look at the line in between. If it's trending in a direction that concerns you, that's a conversation to have directly with your property manager — not something to note quietly and wait to see if it corrects itself.

We recently reviewed a single-unit condo where the tenant was about as good as it gets — $8,500 in rent, paid on time every month, sometimes even a few days early. On paper, that looks like a property with nothing to worry about. But the cash balance still dropped from a $17K opening to $6K by close. The math behind it: a $6.7K mortgage payment, a pricier-than-typical fire and hazard insurance policy, and a driveway capex expense — all landing in the same stretch. Even with reliable rent at the top of what the unit could realistically command, there wasn't enough room underneath to sustain the property. The only real path to recovering the money that had bled out over the years turned out to be selling — which the owner eventually did, at 3.5x the original purchase price. Rent alone was never going to close that gap; the exit was where the return actually lived.

5. Check a simple revenue-to-mortgage ratio

Look at total revenue on your income statement, and compare it to the total mortgage payment — PITI, meaning principal, interest, taxes, and insurance — you're making on the property. How does that ratio look?

Is revenue running 3x, 4x the mortgage payment? That's generally a healthy cushion. Is it closer to 1x — or worse, not even fully covering the mortgage payment on its own? That's a real problem worth addressing directly, not something to let ride for another quarter in the hope it self-corrects.

A weak ratio can point to a couple of different underlying issues, and it's worth figuring out which one you're actually dealing with. Sometimes it's underperformance on the revenue side — which loops directly back to points 2 and 3 above: undocumented expenses eating into margin, or revenue leaking out through unflagged leases and uncollected delinquency. Other times, the property itself is performing fine, but the loan is priced too high for what it can currently support, in which case it may be worth exploring a refinance rather than assuming the property itself is the problem.

Either way, this is a simple enough ratio that any owner can calculate it themselves in a few minutes with a calculator and two numbers already sitting on their own income statement. It's worth doing regularly — quarterly at minimum — rather than once, since a ratio that looks fine in January can quietly deteriorate by the time you check again in July.

Get a second set of eyes on your books

This takes about an hour per property if done diligently on a monthly basis. We know property owners get busy — but the performance of your business always depends on how tightly you hold the leash, and how well you establish checks and controls, even with a third-party property manager.

At Brookeside, we have 5+ years of experience working virtually with rental portfolio holders and property managers across the United States. Talk to us now if you need to make sense of the numbers, want a set of eyes regularly monitoring your property's performance and reporting to you, or need to ensure due diligence and clean, hygienic bookkeeping across your portfolio.

5 Red Flags to Watch for When Your Property Manager Sends You Owner Statements

If you own rental property and someone else manages it day-to-day, your owner statement is often the only window you get into what's actually happening with your money. Most owners skim the bottom line — net income, distribution amount — and move on. That's understandable. You hired a property manager precisely so you wouldn't have to dig through rent rolls and vendor invoices every month. But that same trust is exactly how problems stay hidden for years, sometimes without a single dollar going missing — just quietly mismanaged, undocumented, or left unaddressed until it compounds into something real.

We recently completed a multi-year audit for a portfolio holder with 7 multifamily properties and 35+ units across LA County. The engagement covered several years of records, cross-referencing bank statements, check registers, income registers, rent rolls, and bills against what had actually been reported to the owner. What we found wasn't unusual — it's the kind of thing we see often enough, across different property managers and different markets, that it's worth sharing publicly rather than just filing away as a one-off engagement.

None of what follows requires an accounting background to understand. It requires about fifteen minutes a month, the right five documents, and a willingness to actually look instead of just filing the statement away.

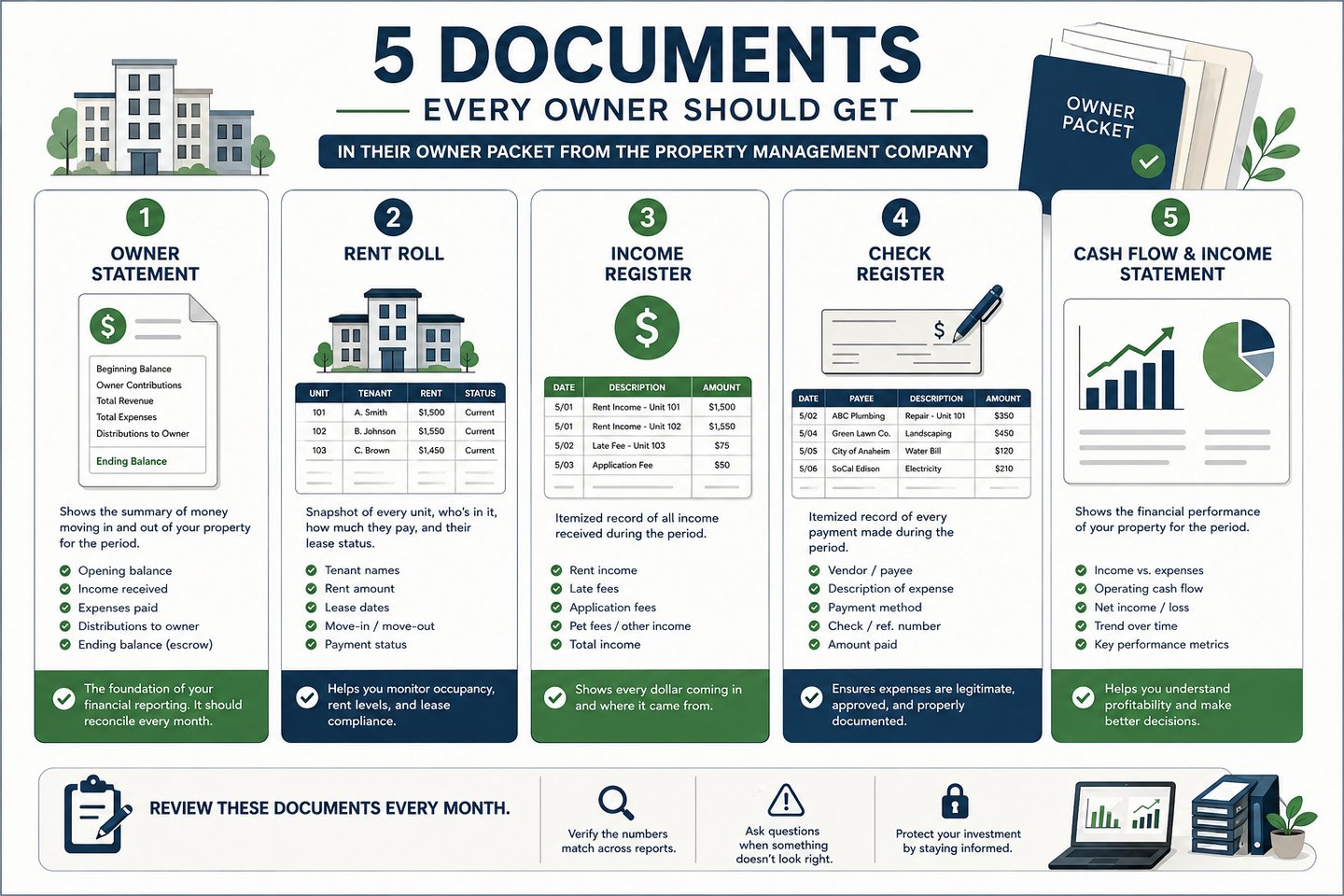

1. Start here: Ask for an Owner Statement

Before you look at anything else — before the income statement, before the cash flow statement — ask your property manager for your Owner Statement. This is the single most important document they should be sending you every month, and it's simpler than it sounds.

At its core, an Owner Statement is just basic addition and subtraction. It should show you:

How much you (the owner) contributed into the property manager's trust or escrow account

How much cash came in as revenue — rent, deposits, and other income

Minus how much cash went out — expenses, vendor payments, repairs

Minus how much was distributed out to you

Equals the closing balance the property manager is holding on your behalf, in escrow

That's it. It's a running explanation of the money moving in and out of your property on your behalf, and it should reconcile cleanly every single month — meaning last month's closing balance is this month's opening balance, with no unexplained jumps in between. If your property manager can't produce this document clearly, on request, in a format you can actually follow, that alone is worth pausing on before you look at anything else.

Beyond the Owner Statement itself, make sure you're also getting the basic supporting records behind it: the rent roll (a snapshot of every unit, who's in it, and what they owe), the income register (every dollar of income, itemized), the check register (every payment made, itemized), the cash flow statement, and the income statement. These are the documents that let you, or anyone reviewing on your behalf, actually verify that the Owner Statement's numbers are real, rather than just trusting the summary at face value.

A surprising number of owners have only ever seen the summary. They've never asked for the underlying registers, and in more than a few cases we've reviewed, those registers either didn't exist in usable form or told a noticeably different story than the summary suggested. You don't need to read these documents every month in full detail. You need to know they exist, that they're available on request, and that someone — you or whoever you bring in — occasionally actually checks that the summary matches the detail.

2. Disbursements with no supporting documentation (expense review)

Every dollar that leaves your property's account should be traceable to an invoice, a work order, or some form of documentation explaining what it was for. Unsupported disbursements — payments with no backup, vague descriptions like "misc" or "repair," or entries that don't match any vendor record — are a red flag regardless of the dollar amount.

This doesn't necessarily mean anything improper happened. Often it's simply sloppy recordkeeping: a bill got paid, the documentation got misfiled or never collected, and nobody circled back to fix it. But here's the uncomfortable truth — sloppy recordkeeping and misuse of funds look identical from the outside. There's no way to tell the difference between an honest paperwork gap and a genuine problem without actually asking for the backup and checking. That's exactly why documentation matters as much as the dollar amount itself.

In practice, this is the core of a basic expense review: pick a handful of disbursements at random, ask for the invoice or work order behind each one, and see how quickly and completely your property manager can produce it. If the answer is "immediately, here you go," that's a good sign about how the whole operation is run. If it takes weeks, or the documentation turns out to be incomplete, that's worth treating as a pattern rather than a one-time hiccup.

3. Expired leases and tenant delinquency with no recovery action (revenue review)

On the revenue side, two things tend to go wrong together, and both are worth checking specifically.

Expired leases that were never flagged. Lease expiration tracking sounds like a small operational detail, but it has real financial and legal consequences. An expired lease that's never renewed, or converted to month-to-month with proper documentation, can create ambiguity about what rent is actually owed, what notice periods apply, and what your legal standing is if a tenant dispute or eviction ever becomes necessary. If your owner statements show steady rental income but you've never been told which leases are up for renewal or already expired, ask. In portfolios we've reviewed, it's not uncommon to find leases that expired a year or more prior with no documented follow-up at all — tenants simply continued paying rent under an agreement that, technically, no longer existed.

Tenant delinquency with no visible recovery action. Delinquent tenants happen — that's a normal part of owning rental property, not a red flag on its own. What's not normal is delinquency that sits on the books month after month with no documented follow-up: no late notices, no payment plans, no eviction filings, nothing. If your owner statement shows a growing "past due" balance but no corresponding narrative about what's being done to recover it, you're not getting the full picture. A balance that's been "past due" for eight months with zero recorded collection activity isn't really an accounts receivable line anymore — it's effectively a write-off that nobody has been honest with you about.

Both of these are, at their core, a revenue review question: is the income you're actually owed being tracked, pursued, and collected — or is it just quietly slipping away by omission, one unflagged lease and one unpursued balance at a time? Neither shows up as a dramatic red number on a summary statement. Both show up, eventually, as revenue that's meaningfully lower than it should be, with no clear explanation why.

Contact

Find us on LinkedIn and Facebook

Phone

contact@brookesideaccounting.services

+1 857-208-7210

© 2025. All rights reserved.

QUERIES