Daily Available Balance Report for Rental Properties: What It Is & Why It Matters

Bank balance and available balance are rarely the same number. For rental property owners managing capital projects, vendor payments, and multiple accounts, knowing the difference isn't optional — it's how you avoid a -$7,000 surprise

FINANCIAL REPORTING

Aditya Kumar

3/18/20266 min read

Daily Available Balance Report for Rental Properties: What It Is & Why It Matters

Bank balance and available balance are rarely the same number. For rental property owners managing capital projects, vendor payments, and multiple accounts, knowing the difference isn't optional — it's how you avoid a -$7,000 surprise.

Why Your Bank Balance Is Lying to You

If you manage rental properties, you probably check your bank balance before making any financial decision. It's a natural instinct — but it's also one of the most common and costly mistakes rental property owners make.

Your bank balance tells you what has already happened. It does not tell you what's coming.

For a single-family landlord with one bank account and a handful of tenants, this distinction might not matter much. But for anyone managing multiple properties, multiple LLCs, active capital projects, vendor payment queues, or revolving lines of credit — the gap between your bank balance and your true available cash can be enormous. And dangerous.

This article explains exactly what a Daily Available Balance Report is, how it works, and why every serious rental property operator in the US should have one updated every single morning.

Bank Balance vs Available Balance: What's the Difference?

These two numbers are frequently confused — and the confusion is expensive.

Bank Balance reflects only transactions that have already fully cleared your account. It shows you the past. Checks you have issued that have not yet been cashed do not appear. EFT payments you have authorised that have not yet settled do not appear. Rent payments in transit from tenants do not appear.

Available Balance is the cash you can actually use right now without creating a problem downstream. It accounts for everything — cleared and uncleared — to give you a true picture of your current liquidity.

The formula is straightforward:

Available Balance = Bank Balance + Pending Deposits − Uncleared Checks

The difference between these two numbers is where poor financial decisions live. A bank balance that shows $9,000 can mask an available balance of under $2,000. Without the calculation, you would never know.

The Core Components of an Available Balance Report

A well-structured Daily Available Balance Report tracks the following for each entity or bank account:

Bank Balance — The current ledger balance as reported by the bank. Starting point only — not the decision-making number.

Pending Deposits — Rent payments, security deposits, or other receipts that have been recorded but not yet cleared. These are money you are expecting but cannot yet spend.

Uncleared Checks — Checks issued, EFTs authorised, or ACH payments processed that have not yet settled against the account. This is the most dangerous blind spot for active operators.

Upcoming Known Obligations — Mortgage payments, utility bills, payroll runs, capital project disbursements, and any other scheduled outflows in the near term. These are not yet uncleared but need to be factored into any decision you make today.

Available Balance — The result after all adjustments. This is the number you make decisions with.

Available Balance After Upcoming Obligations — The most conservative and most useful figure — what you will have after everything known is accounted for.

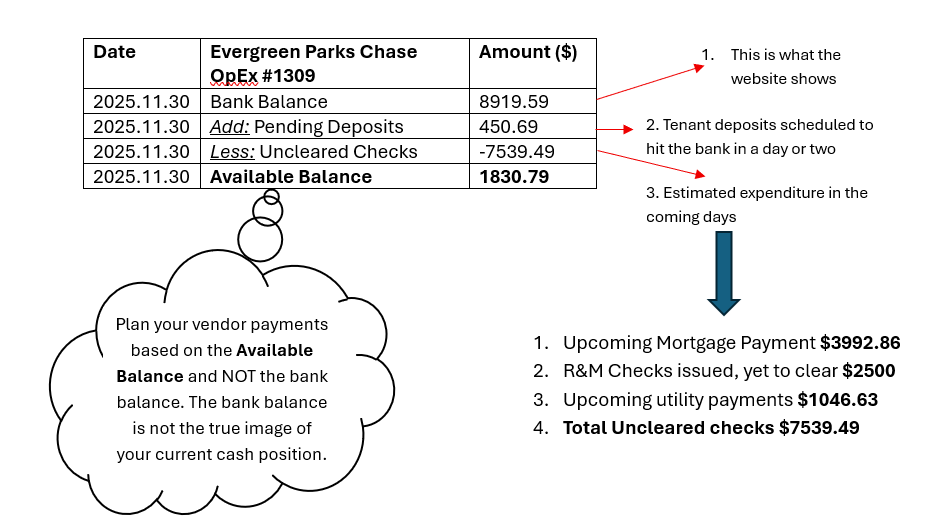

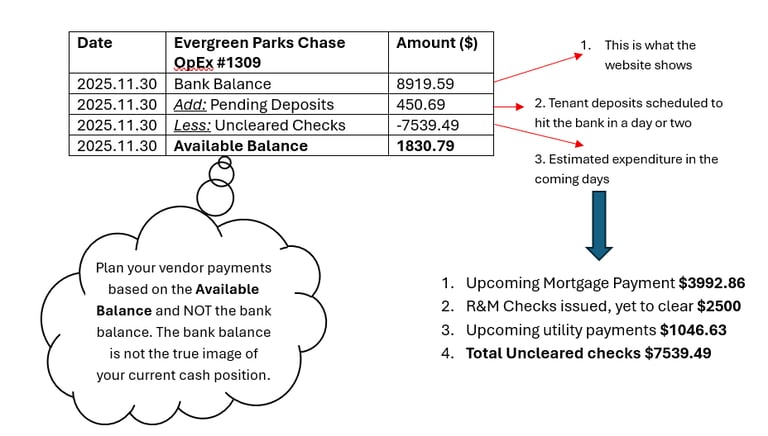

Example 1: The Mortgage Trap

Here is an actual snapshot from a client portfolio:

ItemAmountBank Balance$8,919.59Pending Deposits+$450.69Uncleared Checks−$7,539.49Available Balance$1,830.79

The bank shows nearly $9,000. The actual usable cash is under $2,000.

The uncleared checks in this case included:

Upcoming mortgage payment: $3,992.86

R&M checks issued, yet to clear: $2,500.00

Upcoming utility payments: $1,046.63

Total uncleared: $7,539.49

When the client saw this dashboard, the reaction was immediate: "Ok, so I've got that mortgage coming up — that means I can't transfer funds out right now, correct?"

Correct. The mortgage alone was $3,192. The account needed at least $3,500 to cover it comfortably. The bank balance suggested plenty of room. The available balance told a completely different story.

That moment of clarity — seeing the real number instead of the bank number — is exactly what this report is designed to create. It stops bad decisions before they happen.

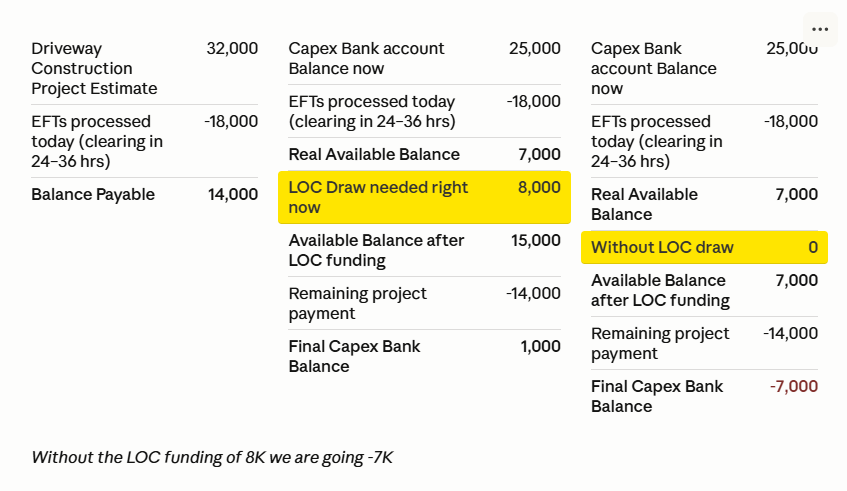

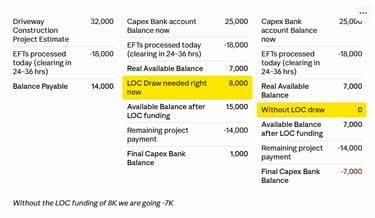

Example 2: The Capital Project Crunch

This scenario plays out regularly for operators managing larger capital projects — and it is where an absent or delayed available balance update can cause serious, expensive damage.

A client operating a Mobile Home Park and RV Park was midway through a driveway construction project with a total budget of $32,000. To keep the project moving, we processed $18,000 in EFT payments to R&M vendors through AvidPay.

Here is what the picture looked like that day:

ItemAmountCapex Bank Account Balance$25,000.00EFTs Processed via AvidPay−$18,000.00Real Available Balance$7,000.00

The bank statement showed $25,000. But for all practical purposes, $18,000 of that was already gone — the EFTs would clear within 24 to 36 hours with no way to reverse them.

With $7,000 in real available cash and $14,000 still needed to complete the project, the client needed to act immediately:

ItemAmountProject Total$32,000.00EFTs Already Processed−$18,000.00Balance Still Payable$14,000.00

We prepared an Income and Expense estimate and sent it to the bank the same day to trigger a draw on the client's revolving Line of Credit — a draw that had been deliberately postponed but could no longer wait.

ItemAmountAvailable Balance Before Draw$7,000.00LOC Draw+$8,000.00Available Balance After Draw$15,000.00Remaining Project Payment−$14,000.00Final Capex Bank Balance$1,000.00

Without that $8,000 LOC draw, this account would have gone $7,000 negative — with vendor payments already in flight through AvidPay and no way to reverse them.

The consequences of missing this would have been severe:

Bounced vendor payments

Stalled construction mid-project

Damaged contractor relationships

An emergency bank call without documentation ready

Potential project delays costing far more than $7,000

Because we were tracking available balance daily, we saw it coming. The Income and Expense estimate was ready, the draw request went out the same morning, and the project continued without interruption.

Why Rental Property Owners Specifically Need This Report

Most small business owners can get away with checking their bank balance once a week. Rental property operators cannot — for several reasons unique to this asset class:

Multiple payment methods create timing gaps. Rent comes in via ACH, check, Venmo, Zelle, and property management portal payments — each with different clearing timelines. A check deposited Monday may not clear until Thursday.

Vendor payments go out through multiple platforms. AvidPay, Gusto, direct ACH, paper checks — each has a different settlement window. Checks can sit uncashed for weeks.

Mortgage payments are non-negotiable and time-sensitive. Missing or bouncing a mortgage payment has immediate consequences — late fees, credit impact, and lender relationship damage.

Capital projects create large temporary cash commitments. A $20,000 EFT to a contractor looks like available cash on your bank statement for 24 to 48 hours. It is not.

Multiple LLCs mean multiple accounts to track simultaneously. Moving money between entities without a clear available balance picture across all accounts is how inter-company transfer errors happen.

The 5 Decisions You Should Never Make Without an Available Balance Report

1. Transferring funds between accounts or entities What looks like surplus cash in one account may have uncleared obligations attached to it. Transferring it creates a shortfall you did not see coming.

2. Authorising a large vendor payment or capital disbursement Before releasing any payment over $1,000, you need to know your true available balance — not your bank balance.

3. Deciding whether to draw on a line of credit LOC draws should be proactive and planned, not reactive and panicked. A daily available balance report lets you time draws intelligently.

4. Telling a contractor or vendor when to expect payment Committing to a payment date based on bank balance when uncleared checks are in flight is how you damage vendor relationships.

5. Evaluating whether to take on a new repair or capital project Before approving any significant expenditure, you need to know not just what you have but what you will have after all current obligations clear.

How Brookeside Accounting Builds This for US Rental Property Owners

As part of our daily bank update process, we maintain a running available balance tracker for each client entity. Every morning, the dashboard reflects:

Current bank balance pulled from your accounting software

All pending deposits — rent, security deposits, reimbursements

All uncleared checks and EFTs across every payment platform

Upcoming known obligations — mortgages, utilities, payroll, capital commitments

Net available balance — the number you actually make decisions with

We work across QuickBooks Online, Buildium, AppFolio, and AvidPay to consolidate this into a single clean view. You do not need to juggle your bank app, your QBO ledger, and your AvidPay queue simultaneously — we do that for you.

The report is sent to you every morning so you start every day knowing exactly where you stand.

The Rule Every Rental Property Owner Should Follow

Never make a financial decision based on your bank balance alone. Always use your available balance.

For rental property owners managing multiple accounts, multiple LLCs, and active capital projects, this is not a nice-to-have. It is the difference between a construction project that stays on track and a $7,000 overdraft that nobody saw coming.

The math is simple. The discipline of doing it every day is what most operators are missing — and what Brookeside Accounting provides.

Want a Daily Available Balance Report built for your portfolio? Book a free consultation with Brookeside Accounting and let us show you what your real cash position looks like.

Brookeside Accounting provides specialised real estate accounting services for rental property owners and managers across the United States, working remotely through Buildium, AppFolio, QuickBooks Online, and Xero.

Contact

Find us on LinkedIn and Facebook

Phone

contact@brookesideaccounting.services

+1 857-208-7210

© 2025. All rights reserved.

QUERIES